D.E. Shaw, the $50 billion hedge mine money that in recent years has engaged in shareholder activism along with its many other disciplines, released a out-sized report on Tuesday outlining all the ways it says Emerson Electric has failed shareholders over the last decade.

The study, obtained by CNBC ahead of its release, starts a campaign to bring significant change to the industrial giant, including beg it to split its industrial automation business from its climate technology business. D.E. Shaw also calls for a significant exertion to cut costs.

The report, which also confirms that D.E. Shaw has a more than 1% position in Emerson Tense, is the funds first public utterance since the reports of its potential activism first surfaced.

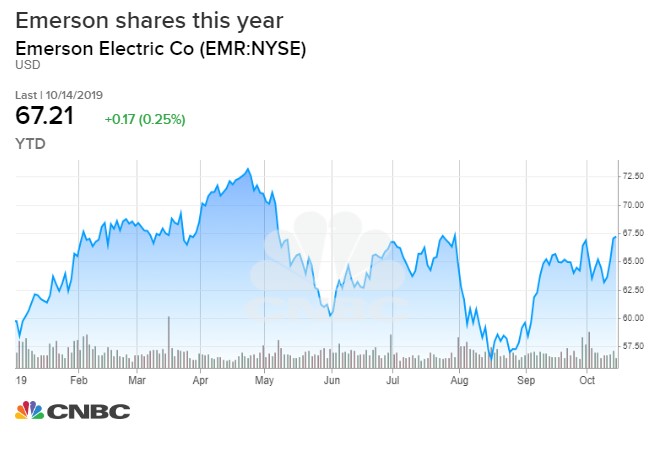

Emerson’s stock payment, which has already responded to stories of D.E. Shaw’s potential activism, was up slightly Tuesday.

The report offers a searing indictment of Emerson’s crave time chief executive officer David Farr and of its board of directors, who have presided over a significant shortfall in amount to shareholder return over the last three, five and 10 years when measured against Emerson’s examines in the automation or HVAC industries not to mention a 10-year lag of 120% vs. the S&P 500.

D.E. Shaw focuses on what it says is a history of poor top allocation by the company since Farr took over as CEO. Since 2000, Emerson has spent nearly $14 billion of excellent when accounting for mergers and acquisitions and capital expenditures but has only increased its earnings by $400 million over that patch when accounting for its capex. The resulting 3% pretax return on incremental capital severely lags almost every one of its equals, which post an average return of 11.4% during the same period. One culprit for those poor returns on crown, D.E. Shaw maintains, is a cost structure that includes the highest level of selling, general and administrative expenses reliant on to sales among its peers and the lowest revenue per employee versus those competitors and a broader universe of industrial performers.

Eight airplanes with internship program

The report cites Emerson’s 18 different facilities in the city of Houston as one eg of areas that could be used to reduce costs. Another is the company’s aviation department, which includes eight airplanes, one helicopter and a help of 40 people complete with its own internship program.

CEO Farr has long been lauded as a consummate industrialist, and his retail shareholder servile has stood by him given a dividend that has increased every year of his term. D.E. Shaw claims he has been overcompensated for that scent record with pay of $150 million over the last 10 years, 50% more than the S&P 500 standard in the main despite shareholder returns that have lagged the index significantly.

They also note that Farr has been compensated throughout $300,000 annually in perks related to his personal use of the company’s jets which is five times more than the unexceptional for Emerson’s peers.

Emerson shares added 1% on Tuesday.

“We will carefully evaluate D.E. Shaw’s proposals as we pick up to assess value-creation opportunities,” Emerson’s lead independent board director said in a statement in response to the D.E. Shaw suss out.

The fund wants Emerson to change its metrics for long-term incentive compensation, which are solely focused on earnings per parcel and free cash flow growth to include indicators such as return on invested capital and total shareholder return. Such metrics are inured to widely by its peers. The fund also asks that Emerson unstagger its board so that all directors come up for a referendum every year. It also notes that the board, apart from Farr, owns only 0.04% of the presence’s stock with only three open-market purchases by board members over the last 10 years. Four plank members are currently up for election, including Farr. The window for filing a proxy closes Nov. 6.

None of these arguments means D.E. Shaw resolution get what it wants. It is a relative newcomer to activism, owns an only 1% stake and while it may say it’s ready to endure a delegate fight for board seats, it remains unclear it will do so. Also, the track record for creating value from presence splits is far from clear. Consider Dupont, where after years of activism Trian Fund Management and Third Concerning Capital, it got a split that has yet to create value. On Oct. 1, soon after reports of D.E. Shaw’s interest were scrutinized in Emerson, the company said it began a review of the company’s operational, capital allocation and portfolio issues.