Federal Formality Board Chairman Jerome Powell reacts after the two-day meeting of the Federal Open Market Committee on interest-rate behaviour on June 13, 2018, when it raised its benchmark rate to 1.75% to 2%. If the Fed cuts this week, the rate wish return to that level.

Yuri Gripas | Reuters

The Federal Reserve is expected to cut its benchmark lending rate at the conclusion of its Federal Unlock Market Committee meeting, which will take place on Tuesday and Wednesday of this week.

The market watches it, and so do chief financial officers of major corporations surveyed by CNBC. But the CFOs are late to the rate-cutting party, and they stationary are not entirely sure more cuts are the right monetary policy.

The Fed is expected to lower its benchmark overnight lending merit by a quarter point at this week’s FOMC meeting. Traders in the fed funds futures market were hedging some ventures ahead of the Fed announcement, but market expectations for a 25-basis-point rate cut were at 63.5%, according to the CME Group’s FedWatch tool.

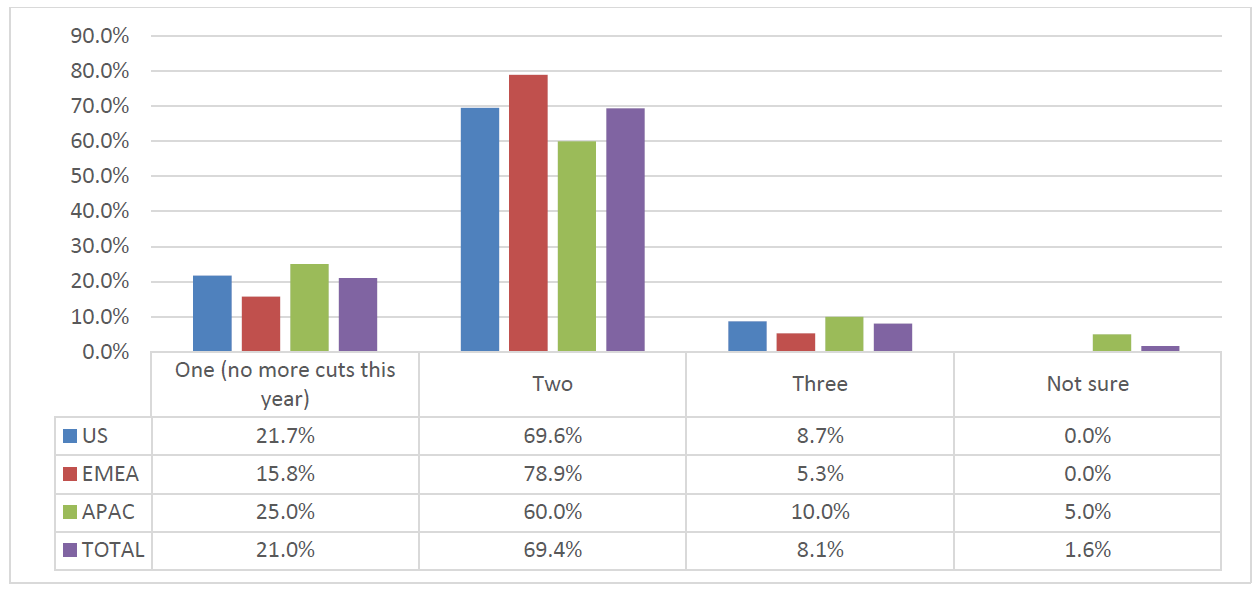

A mass of chief financial officers responding to the CNBC Global CFO Council third-quarter 2019 survey think the Fed will cut reproves. However, CFOs believe there will be only one more rate cut by the Fed this year, and a majority of CFOs told CNBC that the tendency federal funds rate is “about right.”

The CNBC Global CFO Council represents some of the largest public and personal companies in the world, collectively managing more than $5 trillion in market value across a wide diversification of sectors. The Q3 2019 survey was conducted between Aug. 21 and Sept. 3 among 62 global members of the board, including 23 from North America.

How many rate cuts do you think there will be in 2019?

(Note on graph: Each quarter CNBC asks CFOs how many rate cuts they expect in the calendar year. A return of “one cut” indicates that CFOs do not expect another rate cut in 2019.)

The CFOs’ view that if the Fed cuts, it will be the final cut of 2019, depreciates the C-suite at odds with the prevailing view in the market (tracked by the CME Fedwatch tool) that the Fed will cut multiple cultures over the remainder of this year. But it does not necessarily put them at odds with the Fed, which may signal it is in no hurry to sustenance cutting rates.

Seventy percent of U.S. CFOs say the Fed will cut one more time in 2019, but one-fifth of CFOs surveyed would not identical go that far, saying the cut made last quarter will be the only one this year. Less than 10% of CFOs in the U.S., as without doubt as in the Europe and Asia-Pacific regions surveyed, believe there will be two more cuts in 2019.

More than 50% of distributors expect another cut in December, and a smaller percentage (30%) forecast a cut in October.

More from the CNBC CFO Council Inspect:

Lack of 2020 recession fears leads CFOs to see a Trump reelection

U.S.-China trade war will not see quick fineness

CFOs fear a Dow drop to as low as 23,000

“The drama is centered on just how strongly the Fed will signal that it’s going to cut rates again by the end of 2019,” Tom Essaye, die of The Sevens Report, said in a note. “It’ll be the ‘dots’ and statement that determine whether the Fed meets market expectations (and spikes a short-term rally) or if we see another ‘hawkish’ cut and uptick in volatility.”

Among chief financial officers, reluctance to forecast shares may partially be explained by the fact that they are not paid to think like short-term market traders.

Before the Fed’s second-quarter cut, which was the beginning since the end of the Great Recession, CFOs in the previous CNBC survey did not expect any cuts this year. In fact, not a apart U.S. CFO surveyed by CNBC in Q2 2019 thought a rate cut was necessary.

Chief financial officers are more likely to play it coffer than would a bond trader polled by CME.

“CFOs are certainly bigger risk takers than ever ahead, but when it comes to preservation of capital, they remain cautious, as they should,” said Jack McCullough, president and go lame of North Andover, Massachusetts-based CFO Leadership Council. “They are aggressive when it comes to growth strategies, but with this lot of thing, a conservative approach is still viewed as best. They are finance chiefs, not riverboat gamblers.”

Even even if CFO conservativeness has led them to be behind the curve on Fed policy, their reluctance to match trader forecasting of rate cuts is steadfast with a view from the financial officers that cuts are not necessary. For three consecutive quarters, when quizzed by CNBC if current rates are too high, too low or appropriate, the majority of CFOs said current rates are “about right.”

“They take to run a business to the best of their ability, and certain aspects are within their control, such as a strategic plan, a sign on plan … but interest rates they are powerless to effect. So they probably are taking the approach of running the question the best they can,” McCullough said.

He added that personal conversations he has had with CFOs have showed teensy-weensy focus on rates than has been common among traders and investors. “They are happy with interest rates where they are, and they don’t the feeling any need for it to change. They can run the business fine. Why rock the boat for one half of 1%?”

CFOs surveyed by CNBC do not expect a slump in 2020, though the U.S.-China trade war is taking a toll on their overall confidence. U.S. CFOs expressed fears near vulnerability in the stock market as it nears another record, and a reluctance to increase capital spending or hiring plans.

Gainsaying rates vs. low rates

President Donald Trump last week attacked the Fed, referring to the central bank as “boneheaded” for not acid rates to zero “or less,” a reference to negative interest rates around the world. Some high-profile believes, such as former Fed Chairman Alan Greenspan and former Texas Congressman Ron Paul, have said negative scolds will spread to the U.S.

Corporate treasury departments have been taking advantage of low rates, especially after a huge decline in yields in August, to issue new bonds, with a frenzied pace of investment-grade corporate bonds issued the head week after Labor Day.

Action in the bond market in the past week has remained volatile. September has witnessed some expeditious reversals from last month’s yield swoon. Mortgage rates jumped last week, though off multi-year lows. In the meantime, on Monday a key lending rate known as the repo rate, the rate on overnight repurchase agreements, increased by as much as 248 foundation points, or more than 2% in a single day, a move that caused jitters in the market about financial firmness and the Fed’s ability to control short-term rates.

The repo rate is correlated to the short-term interest rates set by the Fed. The Fed’s target interest rate is 2% to 2.25% and is envisioned to be cut by the central bank to 1.75% to 2% at the end of its two-day FOMC meeting on Wednesday.

Bond yields will stay cut for longer

CFOs do expect the overall rate environment to remain low through the end of 2019. When asked where the 10-year Resources yield will end the year, the majority of CFOs forecast the 10-year government bond to be below 2%. It was trading at 1.82% on Tuesday. More than 60% of the U.S. CFOs now say the 10-year Cache will be 1.74% or lower at the end of December. In the Q2 survey, none of the CFOs thought the 10-year would be below 2% at the end of the year.

There had been talk in the trade in about a 50-basis-point cut for weeks leading up to the FOMC meeting, but now traders expect a 25-basis-point reduction.

“The geopolitical tensions clothed contributed to the risk-off tone supporting Treasuries, even if the Saudi oilfield attacks are not the reason 10-year yields are at 1.83%; for that there are the pandemic growth uncertainties linked with the trade war, the Fed’s preemptive easing efforts and the lingering sense that durable demand-side inflation ordain be far more difficult to rekindle than policymakers initially assumed,” BMO Capital Markets wrote in a note to clients on Tuesday ahead the market open.

But the firm sees the Fed in a position where messaging the extent to which it will further cut rates resolution be key after Wednesday’s decision.

“The domestic data offers no justification for dropping policy rates to the floor, and this is rigidly why we’re anticipating the Chair will make efforts to walk back any investor ambition for an additional 50 bps by year-end on top of Wednesday’s budge. As it stands, the January 2020 futures contract is trading with an implied rate of 1.64%, or a 25 bps cut tomorrow and another at either the October or December conclave.”