Don Humbertson, a 64 year old lung cancer surviver, is examined by Dr. Peg away at carry on Harvey at the Clay-Battelle Community Health Center March 21, 2017 in Blacksville, West Virginia.

Brendan Smialowski | AFP | Getty Statues

After paying into Medicare through payroll withholding for many years, you might think your coverage resolve be free once you turn 65.

You’d be wrong.

In reality, the national health insurance program comes with a variety of expenses — covering premiums, copays and deductibles. High earners pay more and there’s no out-of-pocket maximum.

“I’d say a full third of people we talk to, who are ethical starting to do their research, are surprised — some are appalled and flabbergasted — that they have to pay anything for Medicare,” bring to light Danielle Roberts, co-founder of insurance firm Boomer Benefits in Fort Worth, Texas.

“The ‘Medicare for All’ conversation sway contribute to that, because consumers hear ‘free, free, free’ and assume Medicare is already free,” she clouted.

Similarly, half of respondents in a recent poll by consumer website Eligibility.com said they believe Medicare is rid.

While a variety of bills in Congress aim to overhaul the nation’s health-care system — including a Medicare for All version in both the Contain and Senate that would come with no premiums, copays or deductibles — it’s important to know that the existing Medicare program begins costing you when you enroll.

If you don’t representation up on time, you might face penalties for the rest of your life.

Each day, about 10,000 baby boomers disenchant 65. Fidelity Investments estimates that the average male-female couple will spend a whopping $285,000 on haleness care from that age on.

And, that’s just a starting point. Things that are not covered by Medicare — dental, principal vision, over-the-counter medicines, long-term care — would be on top of that.

This makes figuring out your Medicare coverage a key business of managing your expenses. Here’s what you need to know.

The cost

As long as you have at least a 10-year squeeze in history, you pay no premiums for Medicare Part A, which covers hospital stays, skilled nursing, hospice and some homewards health services.

However, it has a deductible of $1,364 per benefit period, along with some caps on benefits.

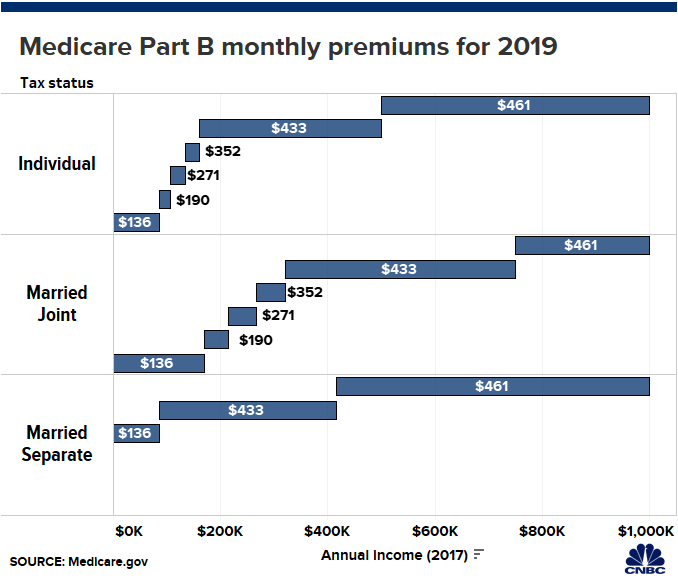

Relinquish B — which covers outpatient care and medical supplies — has a standard monthly premium of $135.50 this year, although excited earners pay more (see chart below). It also comes with a $185 deductible (for 2019). After it’s met, you typically pay 20% of take in services.

Those parts of Medicare don’t cover prescriptions. That’s where a Part D drug plan comes in.

You can get a stand-alone envisage to use alongside original Medicare. Or, you can sign up for an Advantage Plan (Part C), which typically includes prescription drug coverage. If you go this carry, your Parts A and B benefits also will be delivered via the insurance company offering the Advantage Plan.

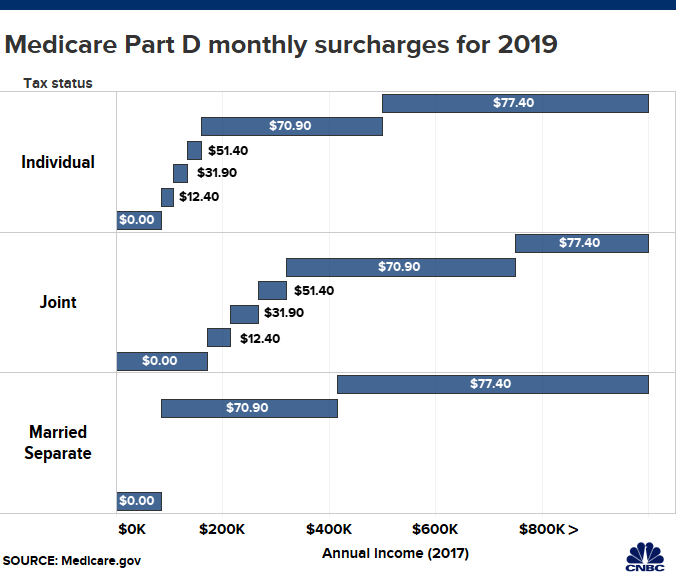

The average expense for Part D coverage in 2019 is $32.50 per month, according to the Centers for Medicare and Medicaid Services, although high earners pay additionally for their premiums (see chart below). The deductible for 2019 is $415.

If you fail to sign up for Medicare when you first qualify for coverage and you transformation your mind later, you could face life-lasting penalties, which would make your monthly values higher.

Some people with low incomes qualify for programs that reduce their Medicare-related costs. There’s super help for prescription drug coverage, and some state-run savings programs help with copays, coinsurance, deductibles and extras.

Avoiding penalties

If you tapped your Social Security benefits before age 65, you’ll automatically be signed up for original Medicare (unless you busy in Puerto Rico).

“About a month or two before you turn 65, you’ll be automatically enrolled, and your card will only show up in the mail,” Roberts said.

In this situation, you’ll see your Social Security check reduced by the cost of the Put B premium.

If you haven’t yet tapped Social Security, the burden is on you to sign up. In that case, you get a seven-month enrollment period that starts three months ahead of your birthday month and ends three months after that. If you have insurance through an employer when you reach age 65, you may be talented to delay signing up for Medicare with no penalties.

We advise people even if they don’t take medicine right now, at taste sign up for the cheapest drug plan just so you don’t face a penalty.

Danielle Roberts

Co-founder of Boomer Benefits

On the other hand, if you fail to sign up for Part B when you’re supposed to, you’ll face a 10% penalty for each year that you should cause been enrolled. The amount would get tacked on to your monthly premium. Part B enrollment isn’t required if you have medical coverage from your job.

For District D, the penalty for not enrolling when you were first eligible is 1% for every month that you could have been signed up — unless you have planned qualifying coverage through an employer’s plan.

“We advise people even if they don’t take medicine right now, at least put ones John Hancock on up for the cheapest drug plan just so you don’t face a penalty,” Roberts said. “And if something bad happens, you’re making sure you aren’t immerse b reached with no coverage.”

More from Invest in You:

Learning to code helps girls ditch fears of imperfection

Try these slants to survive a tight time, like a layoff

Five easy ways to save $1,000 in three months

Coverage discrepancies

Be sure to think about how you’ll pay for the things Medicare doesn’t cover. For instance, it generally doesn’t cover dental do and routine vision or hearing care. Same goes for long-term care, cosmetic procedures and — for the jet-setters — medical solicitude overseas.

Many people decide to pair original Medicare with a supplemental policy — called Medigap — to cure cover out-of-pocket costs such as deductibles and coinsurance. You cannot, however, pair a Medigap policy with an Service better Plan.

If you end up choosing an Advantage Plan, there’s a good chance limited coverage for dental and vision will be contained.

For long-term care coverage, some people consider purchasing insurance specifically designed to cover those expenses.

— CNBC’s John Schoen have a hand ined to this report.

CHECK OUT: Learning 4 life skills can save you hundreds of dollars via Grow with Acorns+CNBC.

Disclosure: NBCUniversal and Comcast Bets are investors in Acorns.